What the Fed rate increase means for your bond mutual funds

There has been a lot of chatter in the markets for months about the Federal Reserve raising rates. Today, they are going up. I want to shed some light on the impact this will have on bonds and bond fund holders over the next few years as it relates to Fed policy.

The risk related to bonds and increasing rates is called duration and interest rate risk. Basically, when interest rates go up, the value of an existing bond goes down. The risk we currently face, based on what the Fed has stated is their plan, is best explained by using an example. To do this, I will use the largest bond fund in the world: Vanguard Total Market Bond Index (VBTLX). This fund has a current yield of 2.36% and duration of 5.72 years. Here is the math behind what the price impact of the Fed’s plan would be on this fund:

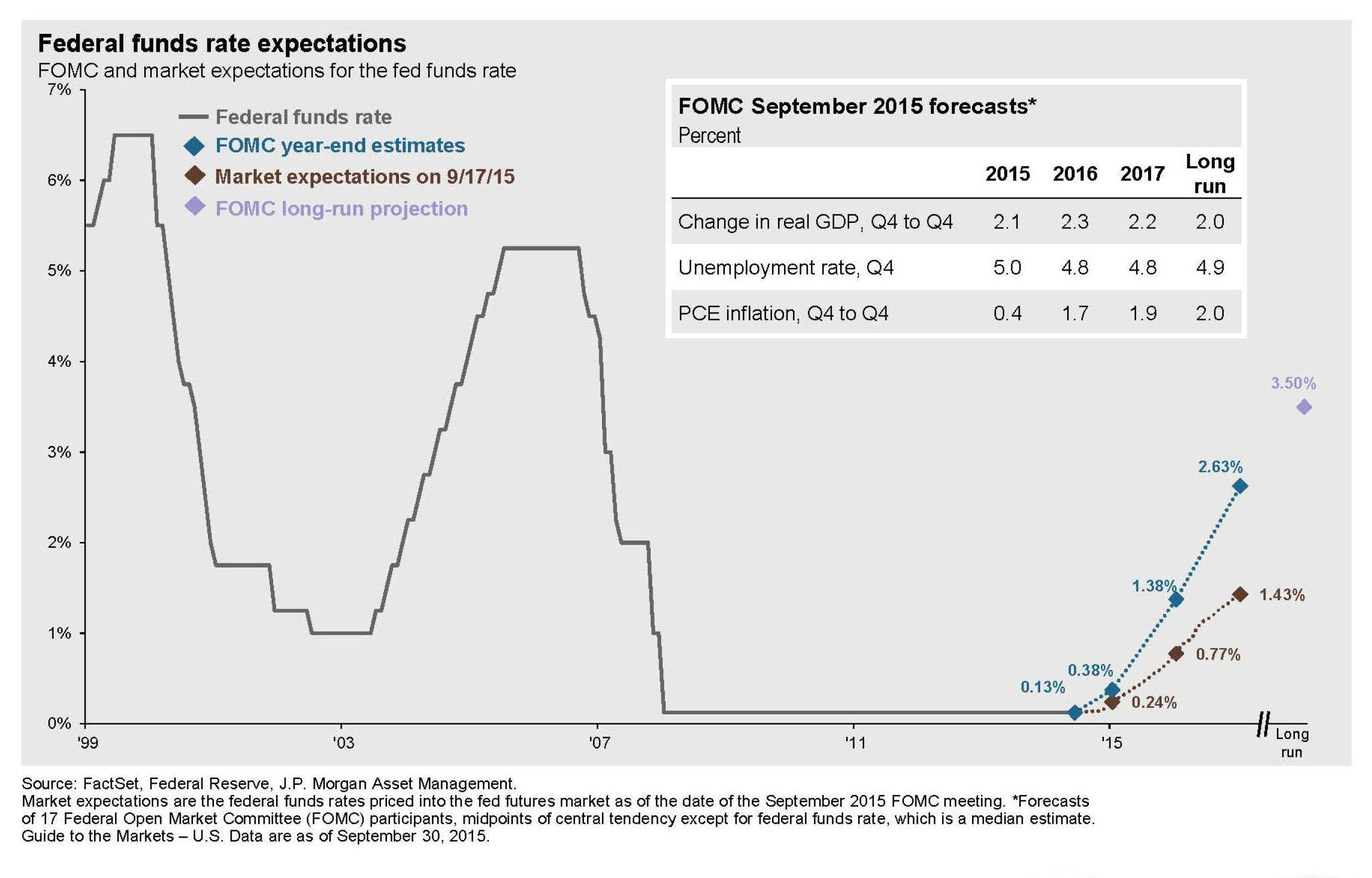

- Fed target rate is 3.50%. The plan is to get there over the next four years, gradually. Take a look at the chart. The Fed rate before the announcement was basically at 0%.

- To calculate price changes, you multiply the rate increase (3.5%) by the duration (5.72%). This equals a -20.02% price change

This calculation implies that VBTLX will decline in price by around 20% over the next four years.

If this occurs as planned over the next four years, the annual impact would be:

-20% divided by 4 years equals -5% per year

-5% minus 2.36% (current yield) equals -2.64% per year

After you factor in the yield, your total return on this fund would be -2.64% per year over the next four years. As rates adjust up this fund will be able to buy some new, higher-yielding bonds to help mitigate some, but not all, of this.

The bottom line is a portfolio of bond funds or bond indexes are not going to produce the same results as they have been over the last ten years. As Fed rates change, different thinking and strategies will be required in order to weather, or even benefit from, this new world going forward. At Windward Wealth we help you put strategies in place to do just that. Please feel free to reach out to me your questions or thoughts.

Gregory Pierce, JD

President & CEO